A N is an Annuity With an Infinite Life Making Continual Annual Payments

Annuities can be optimized for income or long-term growth, but they are not short-term investment strategies. These products appeal to people whose objectives include long-term financial security, retirement income, diversification and principal preservation.

Key Takeaways

- An annuity is an insurance product designed to provide consumers with guaranteed income for life.

- The type of annuity you purchase determines your future annuity payments.

- The primary benefits of buying an annuity include principal protection, the potential for guaranteed lifetime income and the option to leave money to your beneficiaries. Some annuities may also be optimized to help pay for long-term care.

What Is an Annuity?

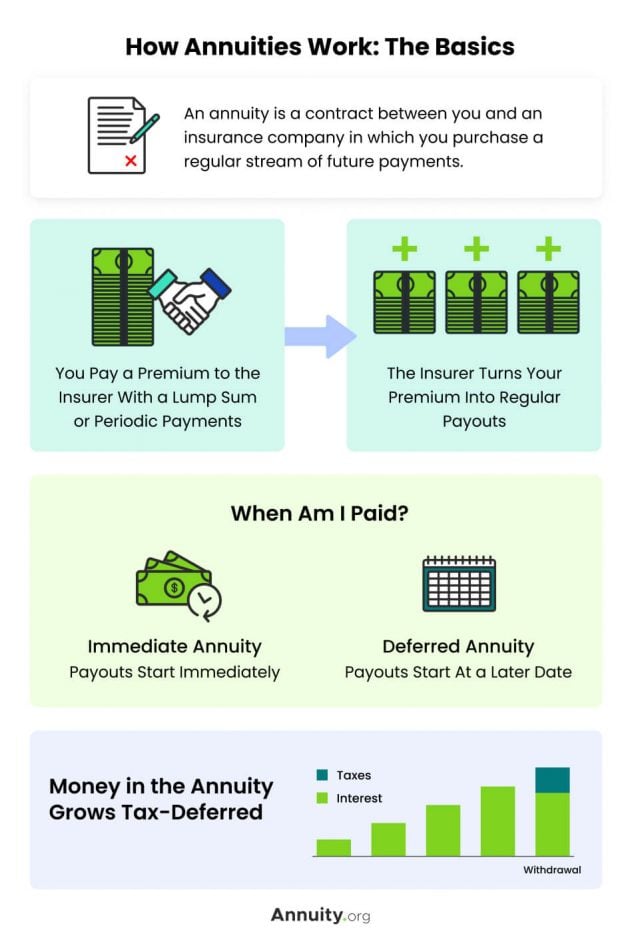

An annuity is a customizable contract issued by an insurance company that converts an investor's premiums into a guaranteed fixed income stream.

More specifically, an annuity contract is a legally binding, written agreement between you and the insurance company that issues the contract. This contract transfers your longevity risk — the risk of you outliving your savings — to the insurance company. In exchange, you pay premiums as outlined in the contract.

Expand

An annuity contract can help you save for retirement or turn your savings into a stream of retirement income.

How Do Annuities Work?

Annuities work by converting a lump-sum premium into a stream of income that a person can't outlive. Many retirees need more than Social Security and investment savings to provide for their daily needs.

Annuities are designed to supply this income through a process of accumulation and annuitization or, in the case of immediate annuities, lifetime payments guaranteed by the insurance company that begin within a month of purchase — no accumulation phase necessary.

In essence, when you buy a deferred annuity, you pay a premium to the insurance company. That initial investment will grow tax-deferred throughout the accumulation phase, typically anywhere from ten to 30 years, based on the terms of your contract. Once the annuitization, or distribution, phase begins — again, based on the terms of your contract — you will start receiving regular payments.

Annuity contracts transfer all the risk of a down market to the insurance company. This means you, the annuity owner, are protected from market risk and longevity risk, that is, the risk of outliving your money.

To offset this risk, insurance companies charge fees for investment management, contract riders, and other administrative services. In addition, most annuity contracts include surrender periods during which the contract holder cannot withdraw money from the annuity without incurring a surrender charge.

Furthermore, insurance companies generally impose caps, spreads and participation rates on indexed annuities, each of which can reduce your return.

Annuities Explained

- Free-Look Period

- Most states require insurance companies to include a free-look period that allows a buyer to cancel the contract without incurring a surrender charge.

- Riders

- Riders are addendums that allow the customization of basic annuity contracts. It's important that you understand the riders you select and are aware of their additional costs.

- Beneficiaries

- You can add a death benefit rider to your contract to ensure that your beneficiary receives a portion of the contract value.

- Fees and Commissions

- The fees and commissions for annuities vary by the type of annuity. Fixed annuities generally have the lowest fees.

- Taxation

- One of the most attractive features of annuities is their favorable tax treatment from the IRS. If your annuity was purchased with money that you've already paid taxes on, then only your earnings will be taxed when the money is withdrawn.

How Are Annuity Rates Set?

Annuity rates are set differently depending on the type of annuity. For example, the issuing insurance company sets the rate of a fixed annuity. They will guarantee this rate for a set period, usually between three and 10 years.

Rate setting is more complicated for other kinds of annuity contracts whose interest rates may vary throughout the term of the contract. A fixed indexed annuity, for example, has both a fixed rate and a rate that's tied to the growth of an equity market index. The indexed rate may be set according to several factors, including rate caps and floors, to keep the rate within a specified range.

How Are Annuities Taxed?

Finance professionals widely recommend annuities to their clients for their tax-deferred growth potential. Once you purchase the annuity, your investment grows tax free for the length of the contract. You won't owe taxes until you receive income payments when the annuity matures.

The part of your annuity payout that is taxed depends on the type of annuity you have. If you own a qualified annuity, you'll pay income taxes on the full withdrawal amount. Meanwhile, only earnings are taxed on non-qualified annuity withdrawals.

Annuities come in two basic configurations: immediate or deferred.

The option you select will depend on your financial goals. If you want to begin receiving annuity payments right away, you will choose an immediate annuity.

Alternately, if you would like to set your payments to begin at some point in the future, you will purchase a deferred annuity and specify the start date in your contract.

-

INCOME NOW

Immediate Annuities

Funded with a single lump-sum payment

Guaranteed monthly payouts

Supplement your retirement savings

Learn More

-

INCOME LATER

Deferred Annuities

Tax-deferred premium growth

Guaranteed lifetime income that begins on the date you specify

More income later because your money accumulates longer

Learn More

Chris Magnussen, licensed insurance agent, explains how much guaranteed income you can expect to receive each month from an annuity.

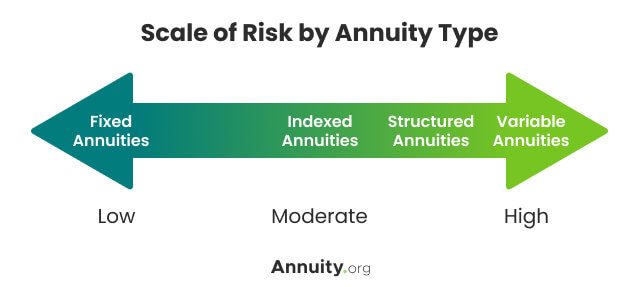

Types of Annuities

Different types of annuities exist to fit the diverse needs of the market. Your personal goals and objectives will determine the type of annuity that is right for you.

Expand

-

GUARANTEED INCOME

Fixed Annuities

Earns a guaranteed rate of interest for a set period of time

Rate of interest may be guaranteed for a set period of time or may fluctuate from anniversary to anniversary

Backed by the insurance company that issued it

Learn More

-

GROWTH POTENTIAL

Fixed Indexed Annuities

Earns interest based on a market index, such as the S&P 500

Doesn't participate directly in the stock market and preserves premium

Guaranteed minimum rate of return

Learn More

-

FLEXIBLE INCOME

Variable Annuities

Earns interest through investments you select within the annuity

Does not guarantee a return but offers more growth potential

Learn More

How soon are you retiring?

What is your goal for purchasing an annuity?

Select all that apply

Reasons To Buy an Annuity

People buy annuities to create long-term income. While most often considered financial solutions for older people who are close to retirement, annuities can benefit investors of any age with a variety of financial goals.

Reasons to buy an annuity include:

- Long-term security

- Tax-deferred growth

- Principal protection

- Probate-free estate distribution

- Inflation adjustments

- Death benefits for heirs

Income annuities are generally suitable for people who are within a year of retirement and want the security of guaranteed income. Remember, single premium immediate annuities (SPIAs) begin paying out within a year of purchase. This means there is no accumulation period as there is with deferred annuities.

For this reason, SPIAs are also beneficial for younger people who have inherited a large sum of money and wish to protect the windfall from poor financial management.

In contrast, deferred annuities are generally not recommended for people who have short-term financial needs or younger people with more aggressive investment strategies.

Wendy Swanson, Retirement Income Certified Professional™, talks about the best time to buy an annuity.

Annuity Benefits

One of the key benefits of an annuity is that it allows the investor to save money without paying taxes on the interest until a later date. Annuities have no contribution limits, unlike 401(k)s and IRAs.

Another significant benefit of annuities is the creation of a predictable income stream to fund retirement. With an annuity, you don't have to worry about outliving your savings. This is a major advantage in the post-pension age.

Your reasons for investing in an annuity should align with your unique lifestyle and financial situation.

-

Tax-Deferred Growth

You save money without paying taxes on the interest until a later date.

-

No Contribution Limits

Unlike 401(k)s and IRAs, you set the dollar amount you invest.

-

Fund Your Retirement

Annuities create predictable income streams for life.

-

Provide for Your Family

Death benefit riders allow you to transfer your money to your loved ones.

How Is My Monthly Income Estimated?

Although it's not possible for an immediate annuity calculator to account for every provision in a contract, our calculator uses a principal amount, a fixed annual interest rate, and your gender and age to generate a rough estimate of what your monthly payments could be for the rest of your life.

We use the gender and age provided along with the Centers for Disease Control and Prevention life expectancy table to estimate the number of years you could receive payments starting one month from when you enter your data.

Disadvantages of Annuities

Some consumers see sacrificing liquidity in return for lifetime financial security as a disadvantage. Indeed, if your financial status or short-term goals limit the amount of cash you have on hand, an annuity is probably not the right solution for you. It wouldn't make financial sense to purchase a valuable, viable product if it's not valuable and viable for you.

Other common concerns about the structure and design of annuities include:

- Commissions and fees

- Complexity

- Conservative returns (as compared with investment products)

- Loss of potential returns from other investments

The loss of potential returns is what's known as "opportunity cost." People frequently cite opportunity cost as drawback. This objection is valid for people with higher risk tolerance. For example, younger investors with longer time horizons would most likely benefit from a more aggressive investment strategy because they have time for their money to grow and could bounce back from temporary market losses.

Older investors and retirees, on the other hand, need to assess opportunity costs as they relate to their specific circumstances. It is less likely that people in this age group would consider opportunity costs a disadvantage of an annuity.

Reduce Your Opportunity Cost

For many investors, the main objection to annuities is the risk of losing access to their money for the length of their contract. This means that in addition to the possibility that you won't be able to cover unexpected expenses, you may miss the opportunity to take advantage of higher interest rates or to invest in the stock market.

This is where your understanding of your long-term goals comes in. Your decision to purchase — or sell — an annuity should be in alignment with your goals, and you should be comfortable with having your money locked down for a modest payout in exchange for guaranteed lifetime income.

To reduce your opportunity cost, consider a partial investment upfront. This will allow you to reserve some of your savings for unplanned expenses and give you the ability to capitalize on a potential rise in interest rates.

Learn more about selling your annuity payments

Annuities vs. Other Fixed Income Products

Annuities are often compared to other fixed income products, including life insurance, certificates of deposit (CDs) and bonds. Let's explore how annuities stack up to these alternatives.

Annuities vs. Life Insurance

While insurance companies issue both products, there are key differences between annuities and life insurance. The major difference is that annuities provide lifetime income for the annuitant with the option to pass on income to a beneficiary after death, while life insurance traditionally serves as a death benefit after the policy holder passes away.

Annuity contracts and life insurance policies are both tax-deferred investment products, and some life insurance policies can grow over time like annuities do. When an annuity matures, the income is usually distributed as a series of payments on a set schedule. Life insurance benefits, on the other hand, are generally distributed in a lump sum to the beneficiary of the policy.

Both products require a premium, which is what you initially pay to purchase the annuity contract or the life insurance policy. However, the way companies determine your premium is different for these two products. Annuity premiums are calculated based on life expectancy, but life insurance premiums are determined by the mortality of the insured.

Because of their differences, a sound financial strategy could include both an annuity and a life insurance policy. Whether one or both products are right for you depends on your long-term money goals.

Annuities vs. CDs

Annuities and CDs are both considered very safe ways to grow your savings over time. Both products provide a guaranteed rate of return over a set period. Annuities and CDs also both favor protecting the investment's principal over aggressive growth.

There are some notable differences between the two products. CDs are short-term investments offered by banks, while annuities are considered more long-term products and are issued by insurance companies. Taxation on an annuity contract doesn't kick in until you withdraw payments, while CD interest is taxed annually.

Annuities are more customizable than CDs because you can choose the terms of the contract and add features like death benefit riders. CDs also tend to offer lower interest rates than annuities because the terms are shorter.

Choosing between an annuity and a CD comes down to how soon you expect to need the money you're investing as principal. Annuities are preferable for long-term savings goals like retirement. CDs, however, are well suited for saving for shorter-term goals such as a house down payment.

Annuities vs. Bonds

Bonds are like annuities in that both are purchased with lump-sum payments and have an established date of maturity. A fundamental difference between annuities and bonds is that annuity contracts are somewhat negotiable, while the terms of bonds are not. You can add benefits or modify terms before you finalize an annuity contract, but a bond indenture cannot be changed.

Annuities also have the advantage of being tax-deferred, while bond income is taxable. In the long term, annuities typically show better rates of return than bonds, and annuities tend to hold their carrying value better over time. The value of bonds tends to decline when interest rates rise.

Bonds and annuities can both be important tools for growing your savings. When choosing which product is right for you, consider the risks and rewards of both financial vehicles and how they align with your own financial priorities.

Annuities in 2022

The economic climate of 2022 has made annuities more attractive than ever for consumers looking to maximize their retirement savings. 2021 saw the highest annuity sales since 2008, with experts citing the financial turmoil caused by the COVID-19 pandemic as a major factor in the record-breaking sales.

In 2022, consumers face the challenge of skyrocketing inflation, which hit a 40-year high in June. Inflation poses a major risk to retirees, as it can erode the purchasing power of their retirement savings. This can be especially problematic if your savings are tied up in low-interest vehicles like bonds or CDs.

Annuities present a few solutions to the problem of inflation. First, the growth rates of annuities, even the more conservative fixed annuities, are typically higher than the returns on products like CDs or bonds.

An annuity can also be helpful for consumers looking to close the "retirement gap," in which your savings and retirement income aren't enough to cover all your expenses in retirement. Annuities offer guaranteed income for the lifetime of the annuitant, and this can help supplement an existing retirement account if those savings are not enough.

One type of annuity is especially good at combating the effects of inflation. An inflation indexed immediate annuity is tied to the movements of the Consumer Price Index, the index used to measure inflation. You can further customize an annuity to hedge against inflation by adding a cost-of-living adjustment rider. This feature increases the monthly payouts of the annuity to keep pace with inflation.

Is an Annuity a Good Investment?

To determine whether an annuity is a good investment, you must consider your personal investment needs and goals. It's also important to account for factors like your age, risk tolerance and lifestyle.

Generally, the younger you are, the more risk you can tolerate. In this case, you might invest in products with greater growth potential. The returns on annuities are modest compared to stocks and other investment vehicles, but they offer guaranteed growth over an extended period.

Annuities tend to be sound investments for older consumers preparing for retirement. The modest returns annuities provide are balanced out by principal protection and tax-deferred growth. Annuities also provide a stream of income you can't outlive, unlike other retirement solutions.

When deciding whether to invest in an annuity, weigh which characteristics of a savings vehicle are most important to you. If you want a safe investment that allows your money to grow tax-deferred and gives you the option to pass on your investment to a beneficiary, an annuity might be the right choice.

How To Buy an Annuity

Annuities are issued by insurance companies, but most contracts are not sold directly to the public from the company's own agents. The majority of annuities in America are purchased from distributors, brokerage firms, banks, mutual fund companies and independent agents.

These distributors will work with you to negotiate your contract and help you manage the contract as your annuity matures. You will primarily work with the agent who sold you the annuity, though you may occasionally receive information from the insurance company that backs the annuity.

Taking the first step towards purchasing an annuity is as easy as contacting us now. We'll put you in touch with one of our trusted partners for more information on securing your financial future.

- Contact Us

We'll route you to a financial expert who specializes in annuities and retirement planning. - Get a Free Consultation

Our trusted network of advisors will listen to you and guide you toward an annuity that will allow you to achieve your goals. - Get Guaranteed Income for Life

Get peace of mind knowing you've made a smart financial decision by securing a reliable income for your golden years.

Chris Magnussen, licensed insurance agent, explains the benefits of working with an independent agent.

Peace of Mind Comes From Knowing Your Money Is Protected

Learn more about how annuities can help provide you with guaranteed income, regardless of market conditions.

Frequently Asked Questions About Annuities

What are annuities?

Annuities are financial instruments that earn interest and provide a guaranteed income stream through payments over a predetermined amount of time. Annuities are often used to fund retirement and come in a variety of types that align with different financial goals and risk tolerance.

How much does an annuity cost?

All annuities share similar fees, but the total cost of an annuity can differ by type. When you purchase an annuity, you pay a premium that can be converted into a fixed income stream. The annuity's administrative fees offset the risks held by the annuity provider, including market volatility. Your contract will outline your financial obligations and the annuity's growth rate.

What are the benefits of an annuity?

Annuities offer a stream of income, provide tax advantages, can grow tax-deferred over time and have no contribution limits. In the event of death, annuities also offer riders that allow you to transfer money to your beneficiaries.

Are annuities safe?

Purchasing an annuity is among the safest options for long-term financial planning. They are insurance products, so they experience less volatility with market fluctuations, although some annuity types have higher risks — and higher potential rewards — than others.

Are annuities insured?

Annuities are insurance products, and annuity providers are often insurance companies. Although the annuity itself is not insured in the literal sense, annuity owners are protected by state guaranty associations if the insurance company defaults on payments.

Do annuities have beneficiaries?

You can designate one or more beneficiaries in your annuity contract if it has a death-benefit provision. The beneficiary would inherit either a specific amount or the remaining money in the annuity.

What is an annuity fund?

When you purchase an annuity, your premium is placed in an investment portfolio called an annuity fund. This portfolio determines the rate of return you'll earn on your annuity.

Source: https://www.annuity.org/annuities/

0 Response to "A N is an Annuity With an Infinite Life Making Continual Annual Payments"

Post a Comment